New Delhi, Dec 6: Gold prices plunged by Rs 215 to close at Rs 12,360 per 10 gram in the bullion market here on poor demand amid weak signals from global markets.

Silver fell by Rs 150 to Rs 16,350 per kg.

Marketmen said reports that the precious metal tumbled in overseas market last evening pulled down its prices here.

Poor demand on ending of marriage season also impacted the sentiments, they added.

Gold in international markets fell after a report showed US employers eliminated jobs in November at the fastest pace in 34 years. A weak trend in crude oil prices was another dampening factor, they said.

In London, gold lost 14.79 dollars to 752.21 dollars an ounce after the US Labour Department said payrolls shrank by 533,000 workers last month.

Standard gold and ornaments plunged by Rs 215 each at Rs 12,360 and Rs 12,210 per 10 gram respectively. Sovereign, lost Rs 50 at Rs 10,400 per piece of eight gram.

Silver ready fell by Rs 150 to Rs 16,350 per kg and weekly-based delivery by Rs 160 to Rs 16,440 per kg. Silver coins, however, held steady at Rs 26,300 for buying and Rs 26,400 for selling of 100 coins.

----------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

----------------------------------------------------------------------------------------------

Saturday, December 6, 2008

Friday, December 5, 2008

Is It Time to Buy Gold?

Just a few months ago, the race was on for gold. In March, gold blew past $1,000 an ounce. Commentators were jumping over each other to make a more attention-getting prediction than anyone else was.

$1,500 an ounce…$2,000…$3,000 – they would say.

The gold bulls were getting very aggressive. Some even started adding a time element to their predictions (i.e. “gold will hit $1,500 an ounce within a year” – that really only happens when bullishness is at an extreme high). I’ve even saw a few - back of the envelope - calculations to justify $10,000 an ounce gold…or higher!

At the time, inflation was a top concern, Wall Street was turning to precious metals in a big way, and gold stocks were setting new highs for the decade.

It was euphoric. Even shares of Seabridge Gold (NYSE:SA) – which just owns a lot of property with gold in the ground – were being bid up every day. The company, which has no sales or revenue, was worth more than $1 billion.

With China’s inflation rate at 12%, Vietnam’s at 20%, Russia’s at 8%, and every other emerging economy facing rampant inflation, the future seemed very bright for gold and precious metals. Expectations of future riches in precious metals were growing stronger by the day. And many gold bugs were eagerly anticipating the big payday that some have been waiting on for 30 years. It was finally going to be “their time.”

Needless to say, it was a very exciting time to be a gold investor. Exciting investments, however, rarely turn out to be all that exciting in the end.

Here we are six months later. Gold price is down 20%, silver prices have been cut in half, and gold investors were met with the financial catastrophe they’ve been waiting for. Stock markets around the world went into freefall, banks failed, real estate values spiraled downward, consumers decided to start saving (all at the same time, practically)…a true financial crisis was at hand.

Gold, as a safe haven, would surely soar, right?

Well…it didn’t, and it probably won’t for a while. Here’s why:

Where, Oh Where, Has My Inflation Gone?

Gold has traditionally provided protection against inflation. I’m sure you’ve heard them all, including: gold is a store of value; gold has been a means of exchange for 3,000 years, etc. Gold has many attributes, which make it attractive.

Of course, detractors can make a decent case against gold. Warren Buffett probably summed the case against gold best when back in 1998 he said:

[Gold] gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.

At the Prosperity Dispatch, we go as far to say gold is not an investment (it’s one of the most commonly misunderstood market myths). Gold is, however, an insurance policy against hyperinflation or economic catastrophe.

But with gold nearing $800 an ounce, is now the time to be buying gold?

Don’t Worry, Be Happy

The answer is yes and no. If you look at gold as an insurance policy and you don’t own any gold, then the answer is yes. However, if you already have gold, then the answer is a bit more complicated.

At its root, inflation is based on the amount of money supply. If there were more paper currencies floating around in the world chasing the same amount of stuff, then naturally things would get more expensive. That’s inflation. But right now, we’re in a period of deflation. Things are a lot cheaper than they were just a few months ago, and everything is getting a lot cheaper.

Just look at the prices for commodities. Zinc and nickel prices are off more than 75%. Copper, aluminum, and iron ore prices are down more than 50%. Fertilizer prices have practically fallen off a cliff. Oil, natural gas…you get the picture.

Deflation is not just in the markets though, you can see it all over in the real world. As we’ve been anticipating for a while, retailers are slashing the price on anything (You can view the original article on how bad the retail downturn will get here.), and they’re only going to keep slashing prices. From their perspective when cash flows are drying up and the bills are piling up, it’s far better to sell a sweater at a loss than have it unsold.

It’s not just prices at the mall though. Gasoline prices have fallen for 77 straight days. The automakers are sponsoring massive discounts (as big as 50% off in some places) just to get their bloated inventories trimmed down. Pretty soon you’ll see the impact of falling oil and energy prices in the form of lower electricity and heating bills.

If anyone who is concerned about inflation now, they simply shouldn’t be. As Jeremy Grantham noted a few weeks ago,

Don’t worry at all about inflation. We can all save up our worries there for a couple of years from now and then really worry!

Printing Presses on Hyperspeed

However, I know why many gold buyers are getting frustrated, as they are constantly barraged about how much new fiat currency is being created.

The Fed is printing dollars at an unprecedented rate, and if the economy doesn’t turn around in the next year or so, the U.S. central bank could be on the hook for trillions more. The only way it can pay for it is with more new dollars.

Therefore, it would make sense, on the surface, that inflation is imminent. Frankly, the risk of inflation down the road will be very real (remember, the Fed can reduce money supply as well). For now though, consumers are dealing with one of the greatest periods of paper wealth destruction of the past century.

Real estate prices have tumbled and still haven’t hit rock bottom. On top of that, the overall stock market has been cut in half. That means about $20 trillion in wealth has been eliminated.

Sure, that was all paper wealth and it was never real money that anyone could spend. But it sure had an impact on consumption. The average consumer who watched his house triple in value over the past few years certainly splurged on a few nice things. And the man whose portfolio just doubled certainly spent a few extra bucks on whatever he wanted when the market was setting new highs.

That’s why despite the trillions of new dollars being thrown into the economy, we’re still in a period of deflation. A lack of inflation will certainly put the brakes on any bull market in gold. That is, if we’re really still in a bull market for gold.

I’ve Never Seen a Bull Market Like This

This is what concerns me most right now about gold. There’s a good chance the bull market may be over. Gold is already down 25% from its March highs and a lot of investors are betting it’s just a correction. I’ve got to tell you, I’ve been through quite a few bull markets and I’ve never seen one like this.

A few months ago, gold shot up $70 an ounce in a day. It was gold’s biggest one-day move in history, but the rally was short-lived. Following the big move, gold prices dropped almost 30% before bottoming out just under $700 an ounce. After all those sharp ups and downs, no one was really surprised when gold would drop $40 in one day and then climb $30 the next, and vice versa.

This is what concerns me, because bull markets are usually much steadier. There’s some volatility, but ups and downs are usually pretty small.

The perfect example is the bull market in fertilizer stocks. For years, stocks like Potash Corp (POT) and Mosaic (MOS) would just steadily climb. Then over the summer, all of the fertilizer stocks doubled in price in about two months time. The bubble started to form and it looked like these stocks would go on forever.

Then in July, fertilizer stocks became precariously volatile. I was watching Mosaic closely (because I had a sizable short position on it), and remember it dropped 20%, rebounded quickly, dropped sharply, and rebounded again, all in a few weeks time. The bull market in fertilizer stock was showing it wasn’t bulletproof after all.

Whether gold goes up or down will depend on many factors. However, with gold at $770 an ounce and as volatile as ever, it’s definitely not a “sure thing” from here.

Investing and trading is in essence a game of risk and reward -.buy low/sell high. The risks of gold falling further are very real. Deflation is the top concern and the price of everything is falling, and gold is not immune.

To win big safely, you have to buy low. Buying low reduces your downside and increases your upside. It’s the only way to get the risk/reward potential in your favor (step one to making a successful investment).

With that in mind, when asked, “Should I be buying gold right now?” The answer, for most of us, is no. Gold, at $770 an ounce, is at a midpoint, and if you’re looking to buy gold, chances are you’ll be able to pick it up a good bit cheaper than you can today.

----------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

----------------------------------------------------------------------------------------------

$1,500 an ounce…$2,000…$3,000 – they would say.

The gold bulls were getting very aggressive. Some even started adding a time element to their predictions (i.e. “gold will hit $1,500 an ounce within a year” – that really only happens when bullishness is at an extreme high). I’ve even saw a few - back of the envelope - calculations to justify $10,000 an ounce gold…or higher!

At the time, inflation was a top concern, Wall Street was turning to precious metals in a big way, and gold stocks were setting new highs for the decade.

It was euphoric. Even shares of Seabridge Gold (NYSE:SA) – which just owns a lot of property with gold in the ground – were being bid up every day. The company, which has no sales or revenue, was worth more than $1 billion.

With China’s inflation rate at 12%, Vietnam’s at 20%, Russia’s at 8%, and every other emerging economy facing rampant inflation, the future seemed very bright for gold and precious metals. Expectations of future riches in precious metals were growing stronger by the day. And many gold bugs were eagerly anticipating the big payday that some have been waiting on for 30 years. It was finally going to be “their time.”

Needless to say, it was a very exciting time to be a gold investor. Exciting investments, however, rarely turn out to be all that exciting in the end.

Here we are six months later. Gold price is down 20%, silver prices have been cut in half, and gold investors were met with the financial catastrophe they’ve been waiting for. Stock markets around the world went into freefall, banks failed, real estate values spiraled downward, consumers decided to start saving (all at the same time, practically)…a true financial crisis was at hand.

Gold, as a safe haven, would surely soar, right?

Well…it didn’t, and it probably won’t for a while. Here’s why:

Where, Oh Where, Has My Inflation Gone?

Gold has traditionally provided protection against inflation. I’m sure you’ve heard them all, including: gold is a store of value; gold has been a means of exchange for 3,000 years, etc. Gold has many attributes, which make it attractive.

Of course, detractors can make a decent case against gold. Warren Buffett probably summed the case against gold best when back in 1998 he said:

[Gold] gets dug out of the ground in Africa, or someplace. Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.

At the Prosperity Dispatch, we go as far to say gold is not an investment (it’s one of the most commonly misunderstood market myths). Gold is, however, an insurance policy against hyperinflation or economic catastrophe.

But with gold nearing $800 an ounce, is now the time to be buying gold?

Don’t Worry, Be Happy

The answer is yes and no. If you look at gold as an insurance policy and you don’t own any gold, then the answer is yes. However, if you already have gold, then the answer is a bit more complicated.

At its root, inflation is based on the amount of money supply. If there were more paper currencies floating around in the world chasing the same amount of stuff, then naturally things would get more expensive. That’s inflation. But right now, we’re in a period of deflation. Things are a lot cheaper than they were just a few months ago, and everything is getting a lot cheaper.

Just look at the prices for commodities. Zinc and nickel prices are off more than 75%. Copper, aluminum, and iron ore prices are down more than 50%. Fertilizer prices have practically fallen off a cliff. Oil, natural gas…you get the picture.

Deflation is not just in the markets though, you can see it all over in the real world. As we’ve been anticipating for a while, retailers are slashing the price on anything (You can view the original article on how bad the retail downturn will get here.), and they’re only going to keep slashing prices. From their perspective when cash flows are drying up and the bills are piling up, it’s far better to sell a sweater at a loss than have it unsold.

It’s not just prices at the mall though. Gasoline prices have fallen for 77 straight days. The automakers are sponsoring massive discounts (as big as 50% off in some places) just to get their bloated inventories trimmed down. Pretty soon you’ll see the impact of falling oil and energy prices in the form of lower electricity and heating bills.

If anyone who is concerned about inflation now, they simply shouldn’t be. As Jeremy Grantham noted a few weeks ago,

Don’t worry at all about inflation. We can all save up our worries there for a couple of years from now and then really worry!

Printing Presses on Hyperspeed

However, I know why many gold buyers are getting frustrated, as they are constantly barraged about how much new fiat currency is being created.

The Fed is printing dollars at an unprecedented rate, and if the economy doesn’t turn around in the next year or so, the U.S. central bank could be on the hook for trillions more. The only way it can pay for it is with more new dollars.

Therefore, it would make sense, on the surface, that inflation is imminent. Frankly, the risk of inflation down the road will be very real (remember, the Fed can reduce money supply as well). For now though, consumers are dealing with one of the greatest periods of paper wealth destruction of the past century.

Real estate prices have tumbled and still haven’t hit rock bottom. On top of that, the overall stock market has been cut in half. That means about $20 trillion in wealth has been eliminated.

Sure, that was all paper wealth and it was never real money that anyone could spend. But it sure had an impact on consumption. The average consumer who watched his house triple in value over the past few years certainly splurged on a few nice things. And the man whose portfolio just doubled certainly spent a few extra bucks on whatever he wanted when the market was setting new highs.

That’s why despite the trillions of new dollars being thrown into the economy, we’re still in a period of deflation. A lack of inflation will certainly put the brakes on any bull market in gold. That is, if we’re really still in a bull market for gold.

I’ve Never Seen a Bull Market Like This

This is what concerns me most right now about gold. There’s a good chance the bull market may be over. Gold is already down 25% from its March highs and a lot of investors are betting it’s just a correction. I’ve got to tell you, I’ve been through quite a few bull markets and I’ve never seen one like this.

A few months ago, gold shot up $70 an ounce in a day. It was gold’s biggest one-day move in history, but the rally was short-lived. Following the big move, gold prices dropped almost 30% before bottoming out just under $700 an ounce. After all those sharp ups and downs, no one was really surprised when gold would drop $40 in one day and then climb $30 the next, and vice versa.

This is what concerns me, because bull markets are usually much steadier. There’s some volatility, but ups and downs are usually pretty small.

The perfect example is the bull market in fertilizer stocks. For years, stocks like Potash Corp (POT) and Mosaic (MOS) would just steadily climb. Then over the summer, all of the fertilizer stocks doubled in price in about two months time. The bubble started to form and it looked like these stocks would go on forever.

Then in July, fertilizer stocks became precariously volatile. I was watching Mosaic closely (because I had a sizable short position on it), and remember it dropped 20%, rebounded quickly, dropped sharply, and rebounded again, all in a few weeks time. The bull market in fertilizer stock was showing it wasn’t bulletproof after all.

Whether gold goes up or down will depend on many factors. However, with gold at $770 an ounce and as volatile as ever, it’s definitely not a “sure thing” from here.

Investing and trading is in essence a game of risk and reward -.buy low/sell high. The risks of gold falling further are very real. Deflation is the top concern and the price of everything is falling, and gold is not immune.

To win big safely, you have to buy low. Buying low reduces your downside and increases your upside. It’s the only way to get the risk/reward potential in your favor (step one to making a successful investment).

With that in mind, when asked, “Should I be buying gold right now?” The answer, for most of us, is no. Gold, at $770 an ounce, is at a midpoint, and if you’re looking to buy gold, chances are you’ll be able to pick it up a good bit cheaper than you can today.

----------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

----------------------------------------------------------------------------------------------

Scary Proposition for AngloGold Ashanti

AngloGold Ashanti (AU) is a South African Gold mining company that should frighten off sensible investors. The company is leveraged just too high with a precarious $1.3 billion of long term debt, and marginal cash holdings of only $400 million. AU's debt load is excessive when compared to its peers, such as Gold Corp's (GG) minimal debt of a mere $10 million. Its liquidity position is less than stellar, and in these volatile economic times, poor liquidity is akin to having one foot on a banana peel and the other on a wet floor.

The shares are overbought: Gold's recent 14% rise from last month's lows has given the shares a jolt. The stock has rallied more than 60%, despite the fact gold has already retraced about one half of its recent gains. The shares have simply gone up too much in too short of a time frame and are due for a heavy dose of profit taking. This ultimate selling pressure should correct the stock back down to a more reasonable $15 to $17 area.

Fundamentals are weak: The company's cost of production shot up dramatically on a sequential basis. It cost the gold producer approximately $434 to mine an ounce of gold in its second quarter, and by its third quarter, AU experienced a 12% increase, to a hefty $486 per ounce. The company is expected to produce 1.25 million ounces of gold in its fourth quarter versus 1.27 million ounces reported in its third quarter. The bottom line is: AU's costs are going up as its production goes down, not a good combination for enhancing profits.

Other produced minerals: The company also produces uranium, copper, sulphur and silver. These minerals are mainly utilized in manufacturing processes, and with a world wide recession in full force, most of these metals have all seen dramatic price collapses due to poor demand. This does not bode well for AU's bottom line.

Recommendation: Take advantage of this overbought situation by exploiting its downside potential. Open a short position with a $23 "buy stop" market order put in place to limit your downside risk. The shares should be covered in the $15-17 area for a juicy profit.

----------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

----------------------------------------------------------------------------------------------

The shares are overbought: Gold's recent 14% rise from last month's lows has given the shares a jolt. The stock has rallied more than 60%, despite the fact gold has already retraced about one half of its recent gains. The shares have simply gone up too much in too short of a time frame and are due for a heavy dose of profit taking. This ultimate selling pressure should correct the stock back down to a more reasonable $15 to $17 area.

Fundamentals are weak: The company's cost of production shot up dramatically on a sequential basis. It cost the gold producer approximately $434 to mine an ounce of gold in its second quarter, and by its third quarter, AU experienced a 12% increase, to a hefty $486 per ounce. The company is expected to produce 1.25 million ounces of gold in its fourth quarter versus 1.27 million ounces reported in its third quarter. The bottom line is: AU's costs are going up as its production goes down, not a good combination for enhancing profits.

Other produced minerals: The company also produces uranium, copper, sulphur and silver. These minerals are mainly utilized in manufacturing processes, and with a world wide recession in full force, most of these metals have all seen dramatic price collapses due to poor demand. This does not bode well for AU's bottom line.

Recommendation: Take advantage of this overbought situation by exploiting its downside potential. Open a short position with a $23 "buy stop" market order put in place to limit your downside risk. The shares should be covered in the $15-17 area for a juicy profit.

----------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

----------------------------------------------------------------------------------------------

Gold and Silver Prices Will Begin to Shine

Although it's not a great consolation, if you've seen your investment accounts implode and your net worth wilt like a rosebud in a desert sun, you can be comforted by the fact that you are not the only one.

Even the great Warren Buffett has seen his "mother lode", Berkshire Hathaway (BRK.A) decline from a 52-week high of $151,650 down to $74,100 a share. It has "recovered" to a recent price of $94,000, still 38% off its high.

Dorothy Kosich, covering the Northwest Mining Association conference on Wednesday in Reno, Nevada, filed the following report with comments from one of the top executives in that industry.

His words reflect the magnitude of the meltdown we have all experienced.

"Never has there been so much money lost in such a short period of time," Franco Nevada (Toronto: FNV.TO) President and CEO David Harquail told an audience at the Northwest Mining Association conference Wednesday.

Nevertheless, Harquail declared," We're expecting gold to go into the thousands" as a monetary expansion generates the "next gold bull market."

The former president of Newmont Capital, Harquail advised that when gold gets re-inflated, expect other commodities to follow.

In his luncheon address to the Northwest Mining Association conference in Reno, Harquail admitted witnessing shock and fear last month in London among the fund managers who had heavily invested in precious metals mining. At the time mining shares were down an average of 72%, major mining companies had been placed on Credit Watch, and mining M&A bids were collapsing.

Molybdenum alone had dropped from $31 to $11 in only two weeks.

Ironically, the earlier timing of when the global economic crisis hit the mining sector and other resource industries could eventually reap some benefit for mining, Harquail suggested. In the meantime, since mining companies could not borrow as heavily as other industries, it may also help the sector's recovery.

Harquail says major mining companies, junior companies and gold are looking better. But, mining exploration may pay the price for the industry's past six months of freefall. [Thursday, companies like Newmont Mining (NEM) and Yamana Gold (AUY) were experiencing a mainly positive day.]

Mining companies with sufficient cash reserves would now rather buy other companies rather than continue to explore or develop new mines. Some are taking advantage of their low share prices to use their cash to buy back their own shares.

And, Harquail noted, some miners are choosing to go private.

Harquail explained that companies without dollars are now operating in survival mode or are actually facing extinction. He referenced examples of as many as six smaller companies considering mergers into a single company.

As a result, Harquail is fearful "that a lot of companies will get out of the exploration business."

Meanwhile, he noted a number of mining and exploration companies won't be able to raise financing for another 18 months.

Nevertheless, Harquail sees a good long-term outlook for a mining industry which has grown accustomed to planning to weather mining's cycles.

Mining's improved stewardship practices have enhanced the reputation of the industry as an investment destination, he said.

Companies also have learned to be able to build cash and diversify. [keep an eye on bell-wether companies like Barrick Gold (ABX) and Goldcorp (GG), as well as Anglogold Ashanti (AU) to see how the most successful companies raise capital, pay off debt, build cash and diversify their operations].

Have you seen the one-year chart of the Market Vectors Goldminers ETF (GDX)? If you are a technical chartist it does appear to have put in a double bottom

However, Harquail is not happy with a U.S. system that has "let a form of casino capitalism" take the domestic mining industry hostage, especially through hedge fund investment. He also joked that the gold mining sector is "overdue for a 15-30 million ounces discovery."

This author isn't convinced that the gold and silver mining industry stock correction is finished yet. However, when we see royalty trusts and "middle men" like Royal Gold (RGLD) and Silver Wheaton (SLW) are trading at prices at the opposite ends of their respective 52-week ranges, one realizes that there is a great deal of confusion and uncertainty over the short term prospects.

I for one will be patient, and hope to pick up more shares of the "best-of-breed" companies whenever they test their recent lows. Without a crystal ball or compelling evidence, it seems foolish to bet too much on a short-term rally with all the current signs of temporary deflation (did you see oil tumble below $43 Thursday?).

It seems prudent to keep enough cash on the sidelines to buy the inevitable dips. Yet I haven't forgotten how far these stocks have fallen already, and that this is the season where gold and silver prices begin to shine.

----------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

----------------------------------------------------------------------------------------------

Gold Demand May Spoil the Party for New Double Eagle

For much of the year, the United States Mint has been touting the upcoming recreation of what it has called the “nation’s most beautiful coin.” Augustus Saint Gaudens’ design for the Ultra High Relief Gold Double Eagle will be recreated as a one ounce 24 karat gold coin available for sale to the public.

The Mint’s intention to recreate the coin was first announced this March, followed by an official unveiling in July, and a well publicized first striking in November. The US Mint intends to strike the coins throughout 2009 in quantities necessary to meet public demand. So far, coin collectors have responded enthusiastically to the upcoming offering. With the recent mainstream attention on gold, there will likely be interest from the broader public as well. Is the United States Mint prepared to handle the potentially significant demand for the new gold coin?

This year the US Mint, as well as most other world mints, have had continuous problems procuring sufficient gold blanks to meet the incredible demand for bullion coins. The US Mint in particular has been forced to suspend sales of some gold bullion offerings and continues to distribute coins though an allocation program since they are unable to meet the full demand.

Next year the US Mint will be at odds with itself as it struggles to meet growing demand for their regular bullion coins and new demand for a potentially hot collectible coin.

To estimate how much demand the new coin might generate, we can look at the US Mint’s 2006 release of the 24 karat American Buffalo Gold coin. Similar to next year’s offering, the coin design was taken from an old collector favorite, in this case the Buffalo Nickel. The coins were offered as one ounce bullion coins and one ounce collector proof coins. Sales of the coins began in late June 2006. In just over six months, the US Mint sold approximately 337,000 bullion coins and 252,000 proof coins for a total of 589,000 ounces worth of gold. Sales of the regular 2006 American Gold Eagle bullion coins totaled only 261,000 ounces.

Even if only the collectible versions of coins are considered, this represents a 50% increase in demand for gold coins. Since the US Mint has been unable to meet the full demand for regular gold bullion coins this year, the prospects that it can handle the additional demand for a popular collectible gold coin on top of already robust gold bullion coin demand seem remote.

Another aspect to consider is that the Ultra High Relief Gold Double Eagles are struck on specialized blanks. The coin will have a thickness of 4 millimeters, which is more than 50% thicker than most one ounce gold bullion coins. So far the US Mint has been procuring these specialized blanks from Gold Corp. (GG), a wholly owned subsidiary of the Western Australian Government, who operate the competing Perth Mint. Notably, the Perth Mint recently announced that it would be forced to cease taking orders for precious metals until January 2009 due to “unprecedented demand.” So, not only will the US Mint need to procure a large amount highly specialized blanks from an already tight market, it will need to procure them from a competitor struggling to meet its own demand.

Taken together, these factors do not bode well for a smooth release of this “recreated materpiece.” I envision a frustrating series back orders, delays, and eventual order limitations for the new coin. The US Mint intended the Ultra High Relief Gold Coin to be “a prestigous example of the highest level of artistic excellence in American coin design.” Instead it might just end up with another gold related headache.

------------------------------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

The Mint’s intention to recreate the coin was first announced this March, followed by an official unveiling in July, and a well publicized first striking in November. The US Mint intends to strike the coins throughout 2009 in quantities necessary to meet public demand. So far, coin collectors have responded enthusiastically to the upcoming offering. With the recent mainstream attention on gold, there will likely be interest from the broader public as well. Is the United States Mint prepared to handle the potentially significant demand for the new gold coin?

This year the US Mint, as well as most other world mints, have had continuous problems procuring sufficient gold blanks to meet the incredible demand for bullion coins. The US Mint in particular has been forced to suspend sales of some gold bullion offerings and continues to distribute coins though an allocation program since they are unable to meet the full demand.

Next year the US Mint will be at odds with itself as it struggles to meet growing demand for their regular bullion coins and new demand for a potentially hot collectible coin.

To estimate how much demand the new coin might generate, we can look at the US Mint’s 2006 release of the 24 karat American Buffalo Gold coin. Similar to next year’s offering, the coin design was taken from an old collector favorite, in this case the Buffalo Nickel. The coins were offered as one ounce bullion coins and one ounce collector proof coins. Sales of the coins began in late June 2006. In just over six months, the US Mint sold approximately 337,000 bullion coins and 252,000 proof coins for a total of 589,000 ounces worth of gold. Sales of the regular 2006 American Gold Eagle bullion coins totaled only 261,000 ounces.

Even if only the collectible versions of coins are considered, this represents a 50% increase in demand for gold coins. Since the US Mint has been unable to meet the full demand for regular gold bullion coins this year, the prospects that it can handle the additional demand for a popular collectible gold coin on top of already robust gold bullion coin demand seem remote.

Another aspect to consider is that the Ultra High Relief Gold Double Eagles are struck on specialized blanks. The coin will have a thickness of 4 millimeters, which is more than 50% thicker than most one ounce gold bullion coins. So far the US Mint has been procuring these specialized blanks from Gold Corp. (GG), a wholly owned subsidiary of the Western Australian Government, who operate the competing Perth Mint. Notably, the Perth Mint recently announced that it would be forced to cease taking orders for precious metals until January 2009 due to “unprecedented demand.” So, not only will the US Mint need to procure a large amount highly specialized blanks from an already tight market, it will need to procure them from a competitor struggling to meet its own demand.

Taken together, these factors do not bode well for a smooth release of this “recreated materpiece.” I envision a frustrating series back orders, delays, and eventual order limitations for the new coin. The US Mint intended the Ultra High Relief Gold Coin to be “a prestigous example of the highest level of artistic excellence in American coin design.” Instead it might just end up with another gold related headache.

------------------------------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

Thursday, December 4, 2008

Peter Schiff on Gold, the Dollar and Asian Markets

Mike Norman, HardAssetsInvestor.com (Norman): Hello everybody, and welcome back for another installment of HardAssetsInvestor.com’s interview series. I’m Mike Norman, your host. Well, he’s back. Mr. Doom and Gloom is here … Peter Schiff, president of Euro Pacific Capital and author of the new book just out, “Bull Moves in Bear Markets.”

Peter Schiff, president of Euro Pacific Capital (Schiff): “The Little Book ...”

Norman: “The Little Book …”; it’s in The Little Book Series. Well look … the last time you were here, things were kind of going your way, but it looks like things have turned upside down.All kidding aside, I know your big thing over the last seven or eight years has been gold. We’re very supportive of gold on this show; we think that probably people should have some gold as part of their overall portfolio mix. But let’s just look at what happened.

Several weeks ago, the U.S. stock market had its worst week in history … even going back to the 1930s … worst week in history. I saw a breakdown of various assets – all assets really – stocks, bonds, gold, commodities, oil. Gold was at the bottom of the list. The top-performing asset, and something that you hate, was the U.S dollar.

So how do you explain that? If we are going through the worst economic and financial crisis in history – precisely what gold is supposed to protect against – why would it perform so bad?

Schiff: Well, I think it will perform very well; you got to give it a little bit more time.

Norman: More time or more decimation?

Schiff: No, what’s happening right now, Mike, is just de-leveraging, and so gold is going down for the same reason a lot of stocks are going down, a lot of commodities are going down. There’s a lot of leverage in this system, there’s a lot of margin calls, a lot of liquidation; a lot of people are having to sell whatever they own to pay off their debts.

Norman: But look at where the money is going … the money is going into U.S. sovereigns, Treasuries … it’s going into the U.S. dollar.

Schiff: For now.

Norman: Why for now?

Schiff: Right now there’s some perception of safety there, but it’s the opposite of the leveraging. If you’re selling your assets, you’re accumulating dollars; but ultimately right now, it’s like there’s been this gigantic nuclear explosion in the United States, and everybody is running toward the blast. Pretty soon they’re going to figure out they’re going in the wrong direction.

Norman: You always talk about gold as a currency, and we have seen currencies appreciate – the yen, for example, the dollar tremendously, for example, but gold has not held up.

Schiff: Well, if you actually look at gold versus other currencies, in the last couple of weeks gold has made new record highs in terms of the South African rand, the Canadian and Australian dollars … so gold was not doing as poorly as many of the currencies, and I think this is all short term.

I think you’re going to see a lot of money moving into gold, and if you look at how much gold has gone down from the peak, the peak was about a thousand … it’s off about 25%. Stocks are off 40%. Gold is still up during this year against the Dow. Norman: Let’s see the performance from this point forward; we’ll look back at this again and we’ll revisit this issue.

Let’s talk about something else, something that you have also … and I just mentioned it … the U.S. dollar. You were very, very negative. In the last month, we have seen unprecedented actions by the U.S. Fed in terms of expansion of the monetary basis; in other words, printing money … what you call printing money … and despite that, the dollar has remained incredibly strong.

How do you explain that according to your logic?

Schiff: Everything the government is doing is inherently negative for the dollar, and all of this…

Norman: It’s not playing out that way.

Schiff: It will; you’ve got to give it time.I remember when I was on television talking about the subprime and people were telling me it’s no big deal, and I said, just wait a while; give it time.

Look, everything that we’re doing – all the bailouts, all the stimulus packages – this is all being financed by inflation. It’s inherently terrible for the dollar.Norman: But you just said yourself that everything is deflating.Schiff: But right now, Mike, you’re getting this de-leveraging, and this is benefitting the dollar, so despite the horrific fundamentals for the dollar, it’s going up anyway.

But ultimately, when this phony rally runs out of steam, the dollar is going to collapse, and that’s when we’re going to have a much greater crisis because now you’re going to have a collapsing dollar, which is going to push long-term interest rates up, commodity prices up.

Norman: I still don’t understand why the dollar is going to collapse. So you’re saying that the Fed is just going to allow … or leave this enormous amount of liquidity in there, that at some point down the road, if we recover, they’re not going Scto take it out?

Schiff: Look, they have no control over it. The Fed is trying to artificially reflate our phony economy, right?

We had this economy that was based on Americans borrowing money and then spending it on products. We have this huge debt finance bubble which is collapsing, and it’s being supported by foreigners.

But when this artificial demand for Treasuries goes away, the Fed is going to try to print a lot of money and the dollar is going to get killed.Norman:I know you've been of this point of view that … just let everything go down, and somehow that's beneficial.

Schiff: It's called capitalismNorman: No, it's not called capitalism. Capitalism has a political structure over it; there are laws, there are regulations.

Schiff: It's all that regulation, all that interference that's the source of our problems. It's the government that interfered with the market; that's why we had a housing bubble, that's why we have this phony economy ― because politicians meddle in the market, and they tried to direct capital in politically favored ways. That's what causes these problems.

Norman: Some people say, basically, Wall Street was given the keys and the government walked away, that it was a totally unregulated environment, and the cutting of regulations to the bone is what precipitated the whole bubble.

Schiff: They gave Wall Street the keys. But the problem is Alan Greenspan, the Fed ― they supplied the alcohol, Wall Street got drunk. It's the government that is responsible, it's the government that supplied the alcohol. If we had sound money and if we didn't have Freddie and Fannie …

Norman: We're going to get to the gold standard in a second, but I have to disagree with you on this, and this is just a fact. The one thing the Fed has control over is the monetary base, and if you look at the last six years ― which, by the way, includes the period when Alan Greenspan was in there supposedly creating all this money ― the monetary base shrunk. In fact, it got down to almost zero growth. We have never seen that, with the exception being periods of recession, but they've [the Fed] been very, very tight.

Schiff: It was showing up in other places. Look at the asset bubbles that they blew up, look how low interest rates were. Maybe they should have been looking at M3 [money supply statistics], but I guess that was growing so much they stopped covering it.

Norman: All right. You say that we'd be better off on a gold standard. I've heard you say that, but yet the trade-off with a gold standard, while yes you can maintain stable prices, the cost is less money. Gold standards are inherently deflationary. How can you not…? Even extreme economists [don't] buy into this idea now.

Schiff: Look, we were on a gold standard until 1971, right? We didn't leave it until then. What gold does …

Norman: FDR made it illegal for Americans to own gold in 1933.

Schiff: But international trade … the dollar was redeemable in gold up until 1971 … so all the currencies were backed by the dollar, which was convertible into gold. What gold does is it puts discipline on central bankers and governments: they can't simply spend money that they don't have, they can't run deficits, so it keeps a limit on the size of government.

Norman: The total value of gold ever mined since the beginning of time is $4.3 trillion. The global economy is $60 trillion. Are you suggesting that we should cut the global economy by what, $56 trillion?

Schiff: Mike, prices adjust downward to reflect the supply of gold; that's fine, and we want prices to fall. As consumer prices fall, that's how standards of living grow. You want money to be scarce. The problem is now it's abundant; there's an infinite amount of it.

Norman: If scarce money creates a deflation, a depression, a collapse of business profits, a collapse in employment, how could you argue that that's a better system?

Schiff: No, Mike, it doesn't do all that; it keeps monetary discipline and it allows a free market to function better when you have sound money. It keeps a better supply of savings and debt, and it allows for economies to grow. Because real wealth is not a function of money creation, it's a function of savings and productivity and capital investment, but you get more of that when you have sound money.

Norman: Well, economics savings equal investment, it's an identity, so if you invest it reduces savings. You save in a forced way; there's that old thing called the paradox of thrift.

Schiff: It isn't a paradox, that's a Keynesian myth.

Norman: Well, he knew what he was talking about. OK, look, let's quickly talk about what's in your book, "Bull Moves in Bear Markets." It's certainly been a bear market; what are the bull moves?

Schiff: Well, they haven't materialized yet but they're going to. I think the bull moves are commodities; I think we're still in a bull market in commodities, particularly precious metals, but I think you buy in to this dip.

Norman: Now, I kind of agree with you, because we've had such a tremendous … and I'm a contrarian, so …

Schiff: I also like … a big part of my book is to play the Asian theme … to play the growth of the Asian consumer, the death of the American consumer.

Norman: Even with the dollar going up, doesn't that restore purchasing power to the U.S. now?

Schiff: For now, but it's going to go away. We're buying a lot of dividend-paying stocks around the world, particularly in Asia. A lot of the stocks are now trading at very low PEs, double-digit dividend yields.

Norman: There you have it. Sorry, Peter; ran out of time. There you have it, folks. We're going to have Peter back; he's always a great guest.

------------------------------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

Peter Schiff, president of Euro Pacific Capital (Schiff): “The Little Book ...”

Norman: “The Little Book …”; it’s in The Little Book Series. Well look … the last time you were here, things were kind of going your way, but it looks like things have turned upside down.All kidding aside, I know your big thing over the last seven or eight years has been gold. We’re very supportive of gold on this show; we think that probably people should have some gold as part of their overall portfolio mix. But let’s just look at what happened.

Several weeks ago, the U.S. stock market had its worst week in history … even going back to the 1930s … worst week in history. I saw a breakdown of various assets – all assets really – stocks, bonds, gold, commodities, oil. Gold was at the bottom of the list. The top-performing asset, and something that you hate, was the U.S dollar.

So how do you explain that? If we are going through the worst economic and financial crisis in history – precisely what gold is supposed to protect against – why would it perform so bad?

Schiff: Well, I think it will perform very well; you got to give it a little bit more time.

Norman: More time or more decimation?

Schiff: No, what’s happening right now, Mike, is just de-leveraging, and so gold is going down for the same reason a lot of stocks are going down, a lot of commodities are going down. There’s a lot of leverage in this system, there’s a lot of margin calls, a lot of liquidation; a lot of people are having to sell whatever they own to pay off their debts.

Norman: But look at where the money is going … the money is going into U.S. sovereigns, Treasuries … it’s going into the U.S. dollar.

Schiff: For now.

Norman: Why for now?

Schiff: Right now there’s some perception of safety there, but it’s the opposite of the leveraging. If you’re selling your assets, you’re accumulating dollars; but ultimately right now, it’s like there’s been this gigantic nuclear explosion in the United States, and everybody is running toward the blast. Pretty soon they’re going to figure out they’re going in the wrong direction.

Norman: You always talk about gold as a currency, and we have seen currencies appreciate – the yen, for example, the dollar tremendously, for example, but gold has not held up.

Schiff: Well, if you actually look at gold versus other currencies, in the last couple of weeks gold has made new record highs in terms of the South African rand, the Canadian and Australian dollars … so gold was not doing as poorly as many of the currencies, and I think this is all short term.

I think you’re going to see a lot of money moving into gold, and if you look at how much gold has gone down from the peak, the peak was about a thousand … it’s off about 25%. Stocks are off 40%. Gold is still up during this year against the Dow. Norman: Let’s see the performance from this point forward; we’ll look back at this again and we’ll revisit this issue.

Let’s talk about something else, something that you have also … and I just mentioned it … the U.S. dollar. You were very, very negative. In the last month, we have seen unprecedented actions by the U.S. Fed in terms of expansion of the monetary basis; in other words, printing money … what you call printing money … and despite that, the dollar has remained incredibly strong.

How do you explain that according to your logic?

Schiff: Everything the government is doing is inherently negative for the dollar, and all of this…

Norman: It’s not playing out that way.

Schiff: It will; you’ve got to give it time.I remember when I was on television talking about the subprime and people were telling me it’s no big deal, and I said, just wait a while; give it time.

Look, everything that we’re doing – all the bailouts, all the stimulus packages – this is all being financed by inflation. It’s inherently terrible for the dollar.Norman: But you just said yourself that everything is deflating.Schiff: But right now, Mike, you’re getting this de-leveraging, and this is benefitting the dollar, so despite the horrific fundamentals for the dollar, it’s going up anyway.

But ultimately, when this phony rally runs out of steam, the dollar is going to collapse, and that’s when we’re going to have a much greater crisis because now you’re going to have a collapsing dollar, which is going to push long-term interest rates up, commodity prices up.

Norman: I still don’t understand why the dollar is going to collapse. So you’re saying that the Fed is just going to allow … or leave this enormous amount of liquidity in there, that at some point down the road, if we recover, they’re not going Scto take it out?

Schiff: Look, they have no control over it. The Fed is trying to artificially reflate our phony economy, right?

We had this economy that was based on Americans borrowing money and then spending it on products. We have this huge debt finance bubble which is collapsing, and it’s being supported by foreigners.

But when this artificial demand for Treasuries goes away, the Fed is going to try to print a lot of money and the dollar is going to get killed.Norman:I know you've been of this point of view that … just let everything go down, and somehow that's beneficial.

Schiff: It's called capitalismNorman: No, it's not called capitalism. Capitalism has a political structure over it; there are laws, there are regulations.

Schiff: It's all that regulation, all that interference that's the source of our problems. It's the government that interfered with the market; that's why we had a housing bubble, that's why we have this phony economy ― because politicians meddle in the market, and they tried to direct capital in politically favored ways. That's what causes these problems.

Norman: Some people say, basically, Wall Street was given the keys and the government walked away, that it was a totally unregulated environment, and the cutting of regulations to the bone is what precipitated the whole bubble.

Schiff: They gave Wall Street the keys. But the problem is Alan Greenspan, the Fed ― they supplied the alcohol, Wall Street got drunk. It's the government that is responsible, it's the government that supplied the alcohol. If we had sound money and if we didn't have Freddie and Fannie …

Norman: We're going to get to the gold standard in a second, but I have to disagree with you on this, and this is just a fact. The one thing the Fed has control over is the monetary base, and if you look at the last six years ― which, by the way, includes the period when Alan Greenspan was in there supposedly creating all this money ― the monetary base shrunk. In fact, it got down to almost zero growth. We have never seen that, with the exception being periods of recession, but they've [the Fed] been very, very tight.

Schiff: It was showing up in other places. Look at the asset bubbles that they blew up, look how low interest rates were. Maybe they should have been looking at M3 [money supply statistics], but I guess that was growing so much they stopped covering it.

Norman: All right. You say that we'd be better off on a gold standard. I've heard you say that, but yet the trade-off with a gold standard, while yes you can maintain stable prices, the cost is less money. Gold standards are inherently deflationary. How can you not…? Even extreme economists [don't] buy into this idea now.

Schiff: Look, we were on a gold standard until 1971, right? We didn't leave it until then. What gold does …

Norman: FDR made it illegal for Americans to own gold in 1933.

Schiff: But international trade … the dollar was redeemable in gold up until 1971 … so all the currencies were backed by the dollar, which was convertible into gold. What gold does is it puts discipline on central bankers and governments: they can't simply spend money that they don't have, they can't run deficits, so it keeps a limit on the size of government.

Norman: The total value of gold ever mined since the beginning of time is $4.3 trillion. The global economy is $60 trillion. Are you suggesting that we should cut the global economy by what, $56 trillion?

Schiff: Mike, prices adjust downward to reflect the supply of gold; that's fine, and we want prices to fall. As consumer prices fall, that's how standards of living grow. You want money to be scarce. The problem is now it's abundant; there's an infinite amount of it.

Norman: If scarce money creates a deflation, a depression, a collapse of business profits, a collapse in employment, how could you argue that that's a better system?

Schiff: No, Mike, it doesn't do all that; it keeps monetary discipline and it allows a free market to function better when you have sound money. It keeps a better supply of savings and debt, and it allows for economies to grow. Because real wealth is not a function of money creation, it's a function of savings and productivity and capital investment, but you get more of that when you have sound money.

Norman: Well, economics savings equal investment, it's an identity, so if you invest it reduces savings. You save in a forced way; there's that old thing called the paradox of thrift.

Schiff: It isn't a paradox, that's a Keynesian myth.

Norman: Well, he knew what he was talking about. OK, look, let's quickly talk about what's in your book, "Bull Moves in Bear Markets." It's certainly been a bear market; what are the bull moves?

Schiff: Well, they haven't materialized yet but they're going to. I think the bull moves are commodities; I think we're still in a bull market in commodities, particularly precious metals, but I think you buy in to this dip.

Norman: Now, I kind of agree with you, because we've had such a tremendous … and I'm a contrarian, so …

Schiff: I also like … a big part of my book is to play the Asian theme … to play the growth of the Asian consumer, the death of the American consumer.

Norman: Even with the dollar going up, doesn't that restore purchasing power to the U.S. now?

Schiff: For now, but it's going to go away. We're buying a lot of dividend-paying stocks around the world, particularly in Asia. A lot of the stocks are now trading at very low PEs, double-digit dividend yields.

Norman: There you have it. Sorry, Peter; ran out of time. There you have it, folks. We're going to have Peter back; he's always a great guest.

------------------------------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

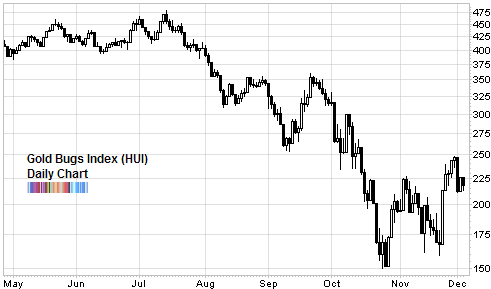

Gold Index Rallies for 65% Gain

Here’s a chart of an index of stocks which recently rallied more than 65%. Can you guess which one it is?

For the answer keep reading…

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

For the answer keep reading…

Here is what I wrote, a few weeks ago, when I taunted the gold bugs, asking “Where is your golden idol now?”

Gold Bugs Index (HUI) has strong support at 175, which would mean the k-ratio to the low 0.20’s and once again, it could set up as a buying opportunity.

That turned out to be a pretty good call, all in all. To be honest though, I didn’t expect such a bombastic rally. Just that the relentless selling would be met with some meaningful support.

By the way, am I being too harsh on the gold bugs? You know, those who believe gold will go to a bajillion dollars and we’ll have to use it for legal tender in some post-apocalyptic “Mad Max” scenario. After all, if gold tops out and craters with the rest of commodities, in the face of one of the most ruthless bear markets and more importantly, in the face of perhaps the harshest global credit and financial crisis we’ve ever faced, when exactly will it rally?

Anyway, I’m sure that folks like Jim Sinclair will come up with some rationale and continue on with the same mindset. It is probably the fault of “manipulators” - just like the stock market is manipulated by the PPT (which by the way, is doing an amazingly atrocious job right now).

Interestingly enough, within the same time period physical gold rallied only 18%, going from a low of $700 per oz. to a high of $825. The previous counter rally in September was a respectable 40% but still a baby compared to this one. I guess my point is that gold and gold stocks are like everything else, supposed to be borrowed for a trade, not married for life. And a good gauge is the trusty k-ratio.

Here are the stocks that make up the Gold Bugs Index (HUI) which their individual weight:

- Barrick GoldABX 16.76%

- Goldcorp IncGG 16.10%

- Newmont MiningNEM 10.41%

- Harmony Gold Mining AdrHMY 6.78%

- Gold Fields Ltd AdrGFI 6.76%

- Kinross GoldKGC 6.43%

- Randgold Resources AdsGOLD 6.07%

- Eldorado Gold CorpEGO 5.52%

- IamgoldcorpIAG 5.41%

- Comp de Minas Buenaventura AdsBVN 4.75%

- Yamana GoldAUY 4.01%

- Agnico Eagle MinesAEM 3.73%

- Hecla MiningHL 2.59%

- Golden Star ResourcesGSS 2.38%

- Coeur d’alene MinesCDE 2.31%

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

The Manipulation of Gold Prices

There is no other leveraged commodity market where short sellers increase their positions, materially, as the price rises, and increase them even more when prices are exploding, except gold and silver. The reason traders don’t normally do that is that it exposes short sellers to unlimited liability and risk. Yet, in both March and July 2008, and on countless occasions over the past 21 years, vast numbers of new gold and silver short positions were temporarily opened up, with the position holders seemingly unconcerned about the fact that precious metals had just risen exponentially, and that there was a very real potential they would bankrupt themselves with unlimited upside potential. Normal traders would not expose themselves to such unlimited risks.

I conclude, therefore, that over the last 21 years or so, “fake” precious metals supply in the form of promises of future delivery have habitually been increased when prices increase until increased “supply” managed to overwhelm increased demand, leading to a temporary price collapse. This is compounded by the fact that the futures prices on COMEX tend to dictate the “officially” report price for the precious metals elsewhere.

After the market is broken, shell-shocked leveraged long market participants have always been thrown out of their positions by margin calls, and/or have been happy to sell contracts back to the short sellers at much lower prices. This process has always allowed short sellers to cover short positions at a profit. If for some reason naked shorts needed to deliver, they could always count on various European central banks (and some say the Fed basement repository) to backstop them, releasing tons of physical gold into the market. It seemed that there were always another 34 tons or so of gold dumped at strategic times to bring down fast rising prices. Meanwhile, huge physical market demand in Asia and severe shortages buffered the downside. Because of the physical demand, prices steadily increased but, perhaps, at a much slower pace than would have been the case in the absence of market manipulation.

Rarely was there ever a serious short-squeeze. Rarely, that is, until Friday of last week when the deliveries demanded by non-leveraged long buyers reached record levels. In spite of an avalanche of complaints from gold and silver investors, the CFTC (Commodity Futures Trading Commission) has never bothered to audit even one vault to see if the short sellers really have the alleged gold and silver they claim to have. There is a legal requirement that, in every futures contract that promises to deliver a physical commodity, the short seller must be 90% covered by either a stockpile of the commodity or appropriate forward contracts with primary producers (such as miners). Inaction by CFTC, in the face of obvious market manipulation, implies a historical government endorsed price management.

Things, however, are changing fast. As previously stated, the first major mini-panic among COMEX gold short sellers happened last Friday. As of Wednesday morning, about 11,500 delivery demands for 100 ounce ingots were made at COMEX, which represents about 5% of the previous open interest. Another 2,000 contracts are still open, and a large percentage of those will probably demand delivery. These demands compare to the usual ½ to 1% of all contracts.

The U.S. economy is in shambles. Both commercial and investment banks are insolvent. European central banks no longer want to sell gold. China wants to buy 360 tons of it as soon as humanly possible, and as soon as it can be done without sending the price into the stratosphere. A close look at the Federal Reserve balance sheet tells us that Ben Bernanke eventually intends to devalue the U.S. dollar against gold. There has been a vast expansion of Fed credit, which has risen from $932 billion to $2.25 trillion in the last two and a half months. The Fed has bought nearly all toxic bank assets that were supposed to be purchased pursuant by the $700 billion Congressional bank bailout.

Official bailout funds have been used to buy equity interests in the various banks instead. By avoiding the use of monitored Congressional funds, the Fed has embarked on a secretive campaign to buy toxic assets. They have refused to give any accounting of their activities, even though they are using taxpayer money to do this. The Fed has refused, for example, to comply with a “freedom of information act” request from Bloomberg News. That refusal is now the subject of a major lawsuit.

The Federal Reserve has embarked on the biggest money printing surge in history, though the world economy has yet to feel its effect. To prevent newly printed dollars from causing immediate hyperinflation, these newly printed dollars have been temporarily sequestered into the banking industry’s reserves, rather than being released for general use. This was done in a number of creative ways.

First, the number of “reverse repurchase agreements” has been increased to $97 billion. A “repurchase agreement” is a non-recourse method by which the Fed increases the money supply by paying dollars for collateral. The collateral, in this case, are toxic defaulting mortgage bonds that banks want to be rid of. The cash enters the system and theoretically stimulates the economy because it supplies banks with money to make loans with.

A “reverse repurchase agreement” is the exact opposite. It is a method of reducing the money supply by selling bonds to the banks, and taking the cash back out of the system. In this case, the Fed gave banks cash for toxic defaulting mortgage bonds. Then, it took the same cash back by selling the banks new treasury bills just received from the U.S. Treasury. The Fed, in turn, bought these T-bills with the newly printed dollars. The banks, having gotten rid of toxic assets, were allowed to transfer private risk to the taxpayers. This process bolsters bank balance sheets by privatizing bank profits, and socializing bank losses.

At the same time, the U.S. Treasury has been very busy selling newly printed Treasury bills to anyone foolish enough to buy them. To a large extent, the fools reside overseas, but some reside inside this country, and the sale of these U.S. bonds has resulted in a substantial inflow of foreign reserves to the Treasury. Banks have also been offered favorable interest rates on both reserve and non-reserve deposits held at the Fed.

This was combined with what is probably a tacit agreement by which the banks were given the money and led to redeposit most newly printed cash back into the Fed, in a category known as “Reserve balances with Federal Reserve Banks”. This category has ballooned from $8 billion in September to $578 billion on November 28th.

On October 9, 2008, the Federal Reserve began paying interest on deposits at Federal Reserve Banks. The overnight rate happens to have dropped way below the “official” federal funds rate. Meanwhile, rates paid by the Fed on required deposits are only .1% less than the federal funds rate, and on voluntary deposits only .35% less than the federal funds rate. Accordingly, U.S. banks can engage in a dollar based one-nation carry trade, which further sequesters the newly printed dollars.

Banks are borrowing from the Fed, then taking the same money, redepositing it, and earning a spread on the interest rate differential. Banks can also deposit newly printed dollars into a category known as “Deposits with Federal Reserve Banks, other than reserve balances.” This category also earns interest in a similar way, and has risen from $12 billion to $554 billion in the same time period. The funds will eventually be used for direct lending from the Fed to open market borrowers, at huge levels of risk that even the free-wheeling cowboys who run things at America’s private banks are not willing to accept.

That being said, most money center banks in America are certainly NOT risk averse, even now. People who are bailed out of foolish decisions never become risk averse. They are, however, very insolvent, and, aside from the non-recourse provisions of Fed repurchase agreements, they would prefer, for bad publicity reasons, not to default on their obligations to the Fed. Aside from the newly printed dollars given to them by the Fed and the recent transfer of all risk to the taxpayers, they have no liquidity of their own with which to make new loans. That is why they aren’t making any. The Fed will eventually make the loans itself and take all the risk, while using the private banking system as merely a means for delivery.

Right now, however, the Fed wants to sequester the new dollars, until the U.S. Treasury has finished the major part of its funding activities. That will allow the Treasury to borrow money at very low rates. The Fed intends to feed money into the system, but at the minimum rate needed to prevent the DOW index from staying under 8,000 for any significant period of time. Right now, most measures are designed simply to stop U.S. banking laws from automatically requiring the closure of most big banks.

The extent of manipulations engaged in by this Federal Reserve is mind numbing. The total number of sequestered dollars has now reached well in excess of $1.2 trillion dollars. That means that Fed credit, so far, has been effectively increased only by about 10%, over the last 2.5 months, rather than 150% that appears on the surface of the Fed balance sheet. The rest is temporarily sequestered.

Back in July, the U.S. Treasury, through the ESF (Exchange Stabilization Fund), sold billions of euros and, I believe, established a dollar sequestering “derivative” by paying interest, perhaps in Euros, to foreign money center banks. This was designed to keep dollars out of circulation, overseas. It was the beginning of the dollar bull back on July 15th.

I had thought, at the time, with good reason, that the U.S. would run out of foreign exchange and would be forced to close down the operation within a few months. I underestimated Ben Bernanke.

Instead, the Fed managed to establish currency swap lines with various foreign nations, under the guise of supplying them with dollars. This need for dollars arose partly as a result of the actions of the Fed, in sequestering Eurodollars in July, and partly as a result of the multiple credit default events which triggered over $2.5 trillion worth of selling in the stock and commodities markets, as 50 to 1 leveraged players were forced to cover about $50 billion worth of credit default insurance obligations.

In truth, the Fed needs the foreign currency more than the foreign central banks need dollars. The Fed is using its new foreign currency resources, in part, to control the value of the dollar, and to insure that U.S. bailout bonds are sold for the highest possible prices at the lowest possible long term costs. Anyone who buys long term Treasury bills is going to lose a fortune of money in the long term.

The Fed has also taken a number of steps beyond those already discussed to restrict aspects of the normal money supply which most strongly affect exchange rates. For example, they only allowed “currency in circulation” to rise by $33 billion in aggregate, while at the same time increasing foreign reverse repurchase agreements to reduce foreign availability of dollars by $30 billion, and reducing the “other liabilities” category dollar availability by another $7 billion. Since it is likely that “other liabilities” involve foreign held dollars, this resulted in a net deficit of $4 billion on foreign exchange markets, as compared to September, 2008.

All these actions, taken together, have supported the dollar overseas, and led to a breakdown of the commodities markets. The adverse effect of a paradoxically rising dollar has been especially severe in dollar dependent commodity producing nations, such as Ukraine.

The net effect is that the U.S. dollar, in spite of terrible fundamentals, is now King of the Currencies once again, at least temporarily. The rising value of the dollar happens also to support naked short sellers of gold and silver, on COMEX, and these are old friends of the Federal Reserve. Supply and demand ultimately determine the price of gold but, in the shorter term, it is inversely tethered to the dollar. When the dollar is artificially high, gold prices will often plunge artificially low.

But, in short, the Fed currently has gained complete control over the value of the dollar. It can now adjust and micromange the dollar on a day-to-day basis. All it needs to do is open and close the “dollar spigot.” When they want the dollar to rise, the Fed can reduce the number of sequestered dollars. When they want it to fall, they simply ease up, releasing dollars into the financial markets. There is only one problem. Real investors are fleeing the stock market, and stock indexes are becoming more and more dependent upon government cash in order to avoid collapse.