Buying physical gold and silver gives the owner definite possession, but comes with high premiums and the necessity to store and protect the metal. This can be done via a bank safe deposit box, but adds to the cost of owning the metal and doesn’t provide total peace of mind for many investors that have lost trust in the banking system. Others might prefer to store the gold on their property, hiding it in the floorboards or purchasing a safe. But this potentially puts you and your family members in harm’s way and again does not offer 100% security.

For investors that prefer not to hold the physical gold, yet place a high value on the safety of their investment vehicle not to default, I recommend the Central Trust of Canada (CEF) or its all-gold counterpart, the Central Gold Trust (GTU). Unlike the popular ETFs such as GLD and SLV, these funds do not lease out your gold and they always maintain 90% or more of assets in unencumbered, segregated and insured, passive long-term holdings of gold and silver bullion. Trace Mayer of Runtogold.com, recently published an article detailing the risk of investing in GLD and SLV. James Turk and others have also covered the unanswered questions about these ETFs in earlier articles.

Setting itself apart from the competition, the stated investment policy of the Board of Directors requires Central Fund to maintain a minimum of 90% of its net assets in gold and silver bullion of which at least 85% must be in physical form. On July 31, 2008, 97.6% of Central Fund’s net assets were invested in gold and silver bullion. Of this bullion, 99.3% was in physical form and 0.7% was in certificate form.

Central Fund’s bullion is stored on an allocated and fully segregated basis in the underground vaults of the Canadian Imperial Bank of Commerce (CM), one of the major Canadian banks, which insures its safekeeping. Bullion holdings and bank vault security are inspected twice annually by directors and/or officers of Central Fund. On every occasion, inspections are required to be performed in the presence of both Central Fund’s external auditors and bank personnel. Central Fund’s chief executive comments:

Our bullion is stored in separate cages, with the name of the owner printed on the cage, and on top of each pallet of bullion it states Central Fund or Central Gold-Trust. This disables the bank from using the asset from any of their purposes. We also pay Lloyds of London for coverage of any possible loss.

Adding to investor peace of mind, CEF has been around since 1961, is based outside of the U.S. (Calgary, Canada) and is run by a board that is respected in the precious metals community, not a bunch of corrupt Wall Street cronies. Demonstrating transparency that is much needed in today’s investment climate, Central Fund makes regular trips to visit the assets and takes their auditors with them. And you get the sense that you are dealing with honest gold investors and not slick marketing or public relations specialists by taking a quick perusal of the CEF website. While they aren’t going to win any design awards, the website is packed with all of the investor information necessary for due diligence.

On the downside, CEF does come with a hefty premium (currently at 16% to NAV). But this premium is less than the premium you are likely to pay on physical bullion, so it is a non-issue for me. And while it is a greater premium than GLD or SLV, I am willing to pay it since I have about as much faith in those ETFs as I do in the Comex.

Tax implications are another deciding factor. Ian McAvity, founding director and advisor to CEF, said there are definite tax advantages to CEF as opposed to an open-ended ETF. Long term gains in the gold ETFs (and presumably Barclays’ silver ETF) would be taxed as collectibles at 28%, according to the Gold ETF prospectus. As a passive foreign investment company with shares not convertible into bullion, CEF is believed to qualify as a passive foreign investment company [PFIC] to enable the 15% capital gains tax treatment, which can be an important factor for investors with long-term ambitions and taxable accounts, said McAvity.

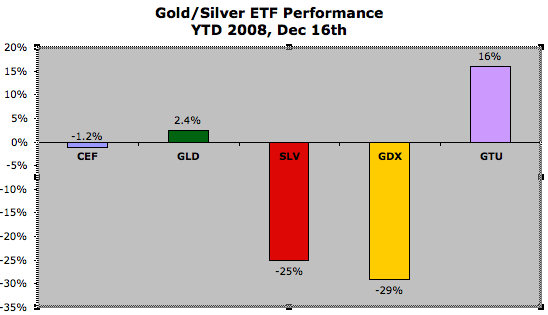

Lastly, we should consider the performance of the various investment options. Year-to-date CEF underperformed by 3 points versus GLD, but this is largely due to the silver exposure. A more fair comparison would be to use Central Gold Trust. GTU significantly outperformed GLD (14 point gap), which should ease any concerns investors have about a higher premium. CEF and GTU offer not only more peace of mind, but better returns compared to the “trust us, the gold/silver is there” approach from iShares or SPDR. It is also interesting to note that the Gold Miners ETF (GDX) is the worst performer year-to-date. This could change as precious metals prices take off in 2009, but I am inclined to park at least half of my gold/silver investments in a safer place than stocks or funds that can’t prove that they actually have physical gold to back my investment dollars. Year-to-date returns are as follows:

click to enlarge

While GTU has outperformed CEF during 2008, I expect silver to outperform gold during the next upleg and thus I own and favor CEF for 2009. Regardless, both of these funds represent sound investment choices during a time when there are fewer and fewer safe places to park your assets. Peace and prosperity to all.

------------------------------------------------------------------------------------------------------------------

GoldTraderAsia.com - Where to Buy and Sell Gold Bullion Bars, Gold Ingots, Gold Coins Collection and Gold Jewellery in Singapore.

To buy Hallmarked 999.9 Pure Swiss Gold Bars, Gold Bullion, Gold Ingots & 916 Gold Coins in Singapore or convert your 916 Physical Gold to physical 999.9 Pure Swiss Gold Bars, Click on Buy Gold Bullion Bars to find out more. You may Sell Gold Bullion Bars to us too.

------------------------------------------------------------------------------------------------------------------

No comments:

Post a Comment